Market Intelligence News & Insights

2024 Funding: A Shift To Stability in Automation Investments

POSTED 11/05/2024

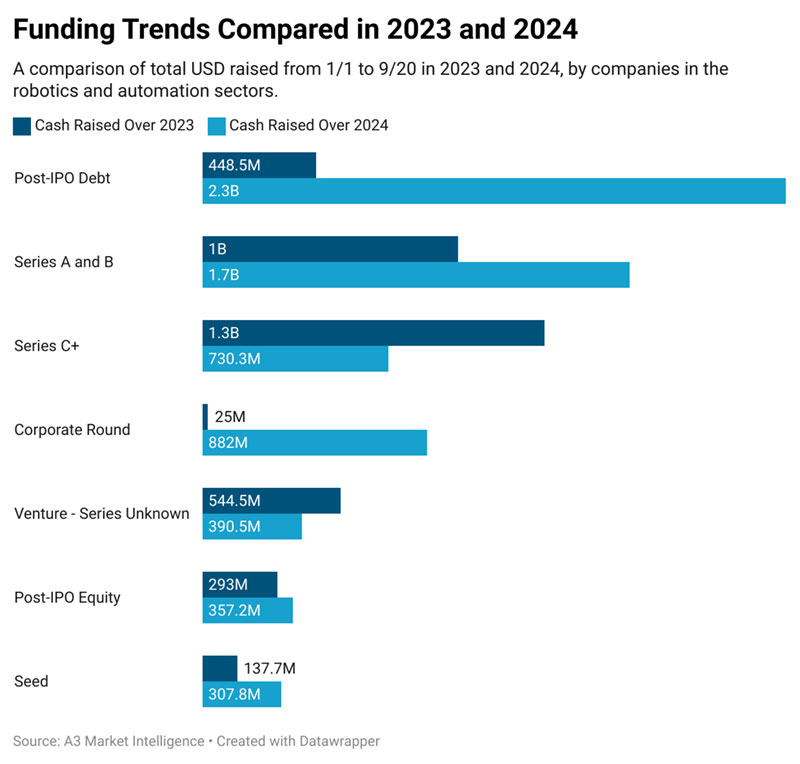

In 2024, the funding landscape for companies in the automation and robotics space reveals a notable shift from higher risk, early-stage investments towards financing for more established companies, according to our dataset of US-based companies in the automation and robotics space.

This trend represents a change towards a more cautious approach, reflecting the broader economic uncertainty and a focus on de-risking into the end of 2024. This article will explore some of these trends observed through the third quarter of this year, as well as some of the potential factors contributing to them.

A Cautious Funding Environment

At the start of 2024, funding rounds for automation and robotics companies exhibited the focus on early-stage dynamism that is to be expected of the startup and venture market. Series A and B rounds saw strong support, with a focus on innovative startups. However, this momentum has markedly slowed into Q3. Recent data indicates a pivot towards debt financing and corporate funding, with even the mix of funding recipients shifting towards established companies.

These patterns illustrate how the funding landscaped has leaned towards lower-risk investment options, with intuitional investors and corporate stakeholders prioritizing the relative stability and more mature market position of established companies over the higher growth and risk of startups. This more conservative stance can probably trace back to the broader economic concerns emblematic of the second half of 2024, along with interest rate uncertainty.

Outliers Skewing the Data

One of the challenges in interpreting this year’s funding data is the presence of large, one-off events that distort the top line figures. A prime example is Lincoln Electric’s $1.5B debt raise, which by itself exceeds the total funding raised across Q3.

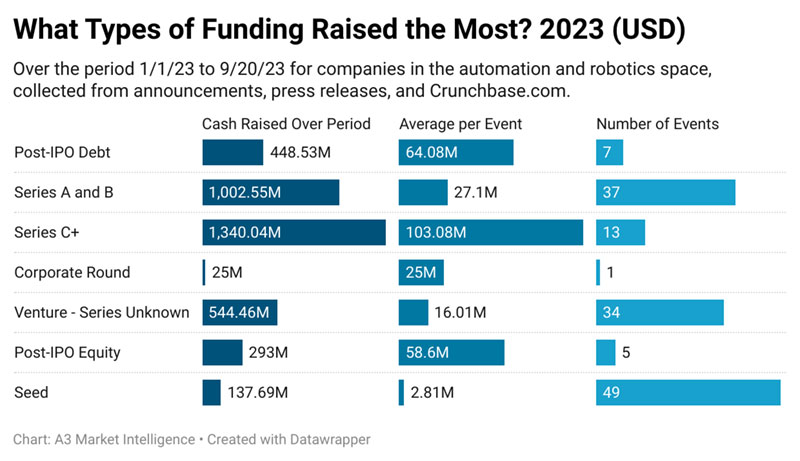

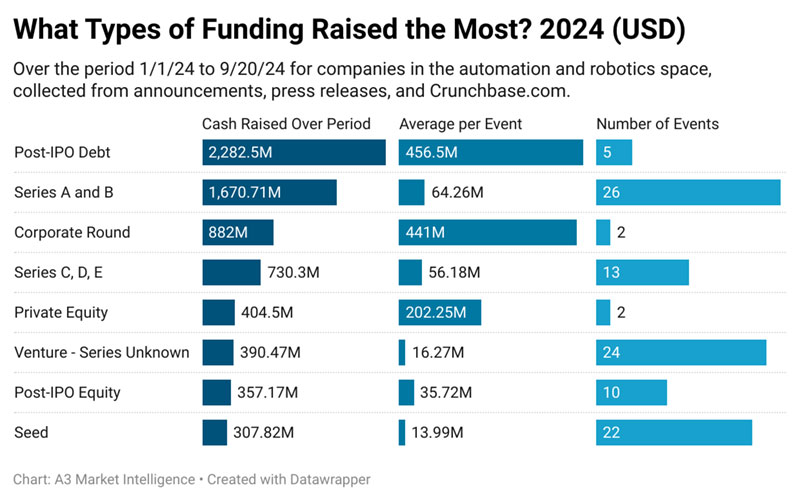

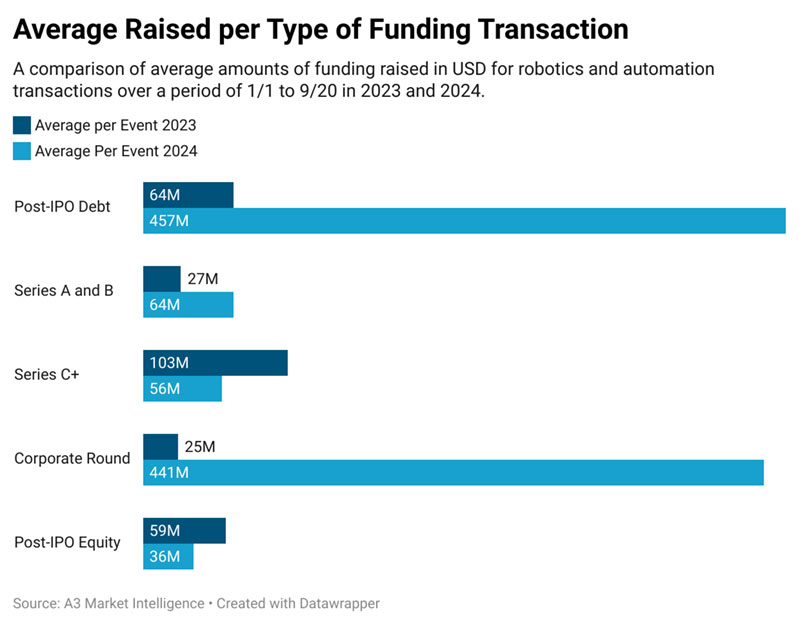

Looking towards averages per funding event, along with the total number of events, 2024 saw fewer funding events but at significantly larger amounts compared to 2023.

Early-Stage Rounds Remain Active but Selective

Despite the slower pace of new funding events compared to early 2024, Series A and B investments remain active, albeit at “higher stakes”, with fewer raises at larger amounts. One standout was Skild AI’s Series A round, which attracted considerable interest. This shows there’s still room for these rounds, particularly for companies demonstrating clear tech advantages or unique market fits.

Key Areas of Investment Focus

Funding in 2024 has increasingly gravitated toward specific segments within automation and robotics, particularly those with clear paths to scaling, profitability, and product/market fit. Notable sectors that have captured investor interest include:

-

Autonomous Vehicles and Delivery: Companies like Cruise and Starship have demonstrated significant traction, driven by the potential to reshape transportation and delivery systems. These firms, including Elroy Air in the air delivery space, have attracted large rounds, often corporate-backed, as they move toward commercialization.

-

Industrial and Warehouse Robotics: The demand for automation in warehousing and logistics has only grown, with firms developing robotic solutions for high-efficiency operations drawing sustained investment. This trend is fueled by continued labor shortages and the push for operational efficiency in supply chain logistics. For more on technologies shaping this space, check out A3’s reports on AMRs and AGVs, as well as our report on Humanoid Robots.

-

Service, Humanoid, and Household Robotics: Consumer-facing robotics, such as humanoid and household service robots, are an emerging focus as companies aim to cater to changing consumer preferences and demand for automated assistance in daily life. Although less prominent than industrial applications, this category is growing steadily and capturing the interest of venture funding.

-

Robot Software and Manufacturing Equipment: Software platforms enabling seamless operation, data collection, and task management for robotics systems continue to secure funding. Companies providing manufacturing and industrial equipment, particularly in the food and beverage industry, have shown potential as automation integrates deeper into traditionally manual sectors. Additionally, this sector is seeing promise in the machine vision space as well, as detailed in our Machine Vision report, available now.

Data Considerations and Limitations

These insights are drawn from funding announcements made between January 1 and September 20, 2024. The dataset excludes the final days of Q3, and manual adjustments were made to remove clear misclassifications. This analysis, therefore, represents a snapshot rather than a comprehensive view, with large single events having an outsized effect on averages.

Conclusion

The automation and robotics sector is evolving within a financially conservative climate, where debt and corporate funding have become primary vehicles for growth. This shift reflects investor caution, focusing on stable returns from established companies while keeping a selective watch on early-stage innovators. Looking ahead, how these funding trends evolve will depend largely on macroeconomic conditions and the ability of early-stage companies to present compelling value in a challenging economic landscape.