News

The Bot Brief

"There is no force on earth more powerful than an idea whose time has come."

- Victor Hugo

Bots In the News:

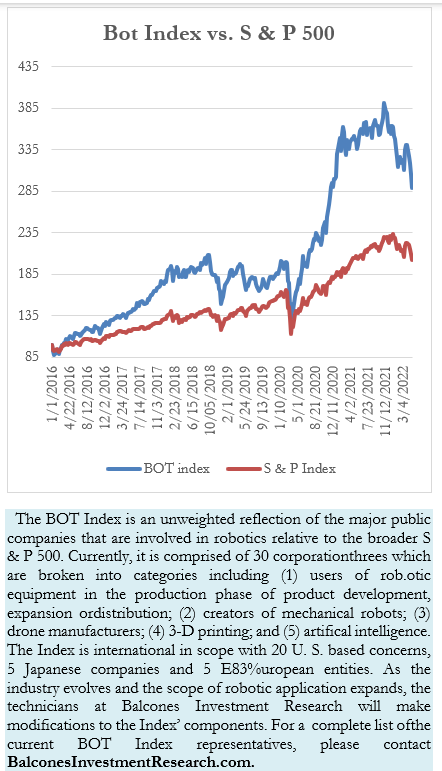

Meteorologically March was to ‘come in like a lion and leave like a lamb’. All we can hope is that, financially, April, who came in like a lion…eating up paper profits, will leave like a lamb for a better May. This final week of the disastrous month saw the Bot Index decline another 5.35% while the S & P 500 fell 3.27%. Not only has the Bot Index peaked in early November of 2021 and has fallen over 100 points, the gap in performance between the bots and the broad market has narrowed.

Leading the weakness of the Bot Index were double digit declines by Amazon (-13.9%), Tesla (-13.36%), Accuray (-19.39%), Oceaneering International (-16%), Faro Technologies (-24.42%) and 3D Systems (-15.18%).

The Index held only four stocks that gained ground during the week. Lincoln Electric led the charge with a 3.59% advance. iRobot rose 2.78%, Textron gained 2% and Immersion Corp. improved by 1.52%.

A Word About the Markets:

It is said that what is past is prologue or as George Santayana stated, "Those who cannot learn from history are doomed to repeat it.” Certainly, this is coming true today as we note the parallels between the current period and the 1970’s. Those of us that are old enough to recall in that period we were suffering from the humiliation following the 1975 fall of Saigon and the retreat of our troops and personnel from South Vietnam. We are suffering the same appearance of weakness in our withdrawal from Afghanistan after a 20-year involvement that ended in failure.

The 1973 oil embargo by the OPEC nations caused a massive increase in gas prices and their availability. We have recently seen the price of a barrel of oil rise to over $100 WTI crude from an average of $39.68 as recently as 2020. Whether it is the war in Ukraine or a self-imposed fossil fuel embargo by Washington is irrelevant to this discussion, the fact is that there is a strong parallel between the two periods. In the 1970’s, consumers rushed to purchase Volkswagen beetles due to their milage while currently there is a long waiting list for electric vehicles.

Get the Training You Need for a Safer Workplace!

Autonomous mobile robots are one of the fastest-growing segments of the robotics industry. During this live virtual training, you'll be introduced to safety protocols and best practices for working with mobile robots in industrial settings.

Learn more and register now for upcoming training dates.

Inflation was rampant in the 1970’s as it is today. Contributing to inflation was the aggregate budget deficit which climbed to 3.9% of the GDP by 1975 from .3% in 1970. Today, the deficit to GDP jumped from 4.6% in 2019 to 15% in 2020 and 12.1% in 2021. The 1970’s Fed policy required tightening to overcome the fiscal spending from the Vietnam war and the social policy cost of The Great Society. Interest rates in both periods reflect the restrictive Fed policies.

Incidentally, there were two significant recessions in the 1970’s and, in concert, the first quarter of 2022 saw a surprise 1.4% decline in the GDP. It is, therefore, consistent to consider that the current investment markets may well perform in a similar fashion to those of the 1970’s. Keep in mind that the government raised capital gains taxes 5 times during the 1970’s to a maximum of 39% at the Federal level. Are tax increases expected in the next several years as the government seeks to accommodate its fiscal needs? Quite likely and the impact to the stock markets in the 1970’s was that the Dow Jones Industrials entered the decade at the same level as the decade ended. Consequently, it was a lost decade for investors. Let us hope that we can learn from history before we too enter a period of little to no secular increase in the investment markets.

Member: American Economic Association, Society of Professional Journalists, United States Press Association. Institute of Chartered Financial Analysts, Robotic Industries Association, Member IEEE.

Bot Brief is a weekly newsletter designed for economists, investment specialists, journalists, and academicians. It receives no remuneration from any companies that may from time to time be featured in the brief and its commentaries, analysis, opinions, and research represent the subjective view of Balcones Investment Research, LLC. Due to the complex and rapidly changing nature of the subject matter, the company makes no assurances as to the absolute accuracy of materials presented.

(5).png)

Balcones Investment Research

Investment Research and publication of The Bot Brief.

Discover how Balcones Investment Research can support your automation journey with their complete range of solutions and expertise.

Visit Company Website

IACET Reaccreditation Demonstrates Yaskawa Motoman’s Commitment to Industry

The International Accreditors for Continuing Education and Training has awarded Yaskawa Motoman the prestigious Accredited Provider accreditation for an additional five years. IACET Accredited Providers are the only organizations approved to offer IACET Continuing Education Units.

Weekly Bot Brief Newsletter on Robotics 7/3/2020

The Bot Index surged 7.33% during the Fourth of July shortened week and again exceeded the 4.02% increase of the...